A group of students from the Department of Financial Accounting, under the supervision of Anna Waldner, conducted a study in cooperation with the Federal Association of Austrian Accountants (BÖB), in which the current status of sustainable action and sustainability reporting at BÖB member companies was surveyed.

A comprehensive standardised online questionnaire was created to determine the status of sustainable action and sustainability reporting. This questionnaire was completed by 48 BÖB members.

The results show that awareness of various laws, standards and guidelines on sustainability reporting is currently relatively low. 41.67% stated that they were not aware of any of the 12 regulations listed, such as the EU Taxonomy Regulation or the Corporate Sustainability Reporting Directive. This knowledge deficit should be counteracted through increased professional training.

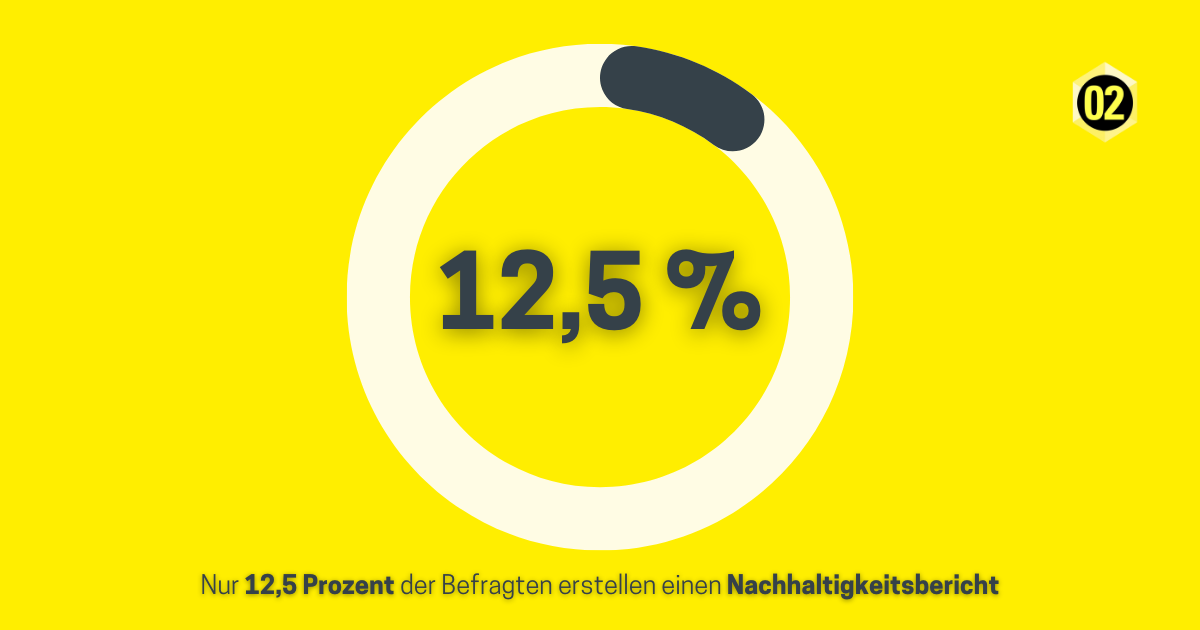

Only 12.5% of the companies in which the survey participants work prepare a sustainability report, with two-thirds doing so voluntarily. The status of sustainable action and sustainability reporting is shown in the following graphic: Infographic for sustainability report

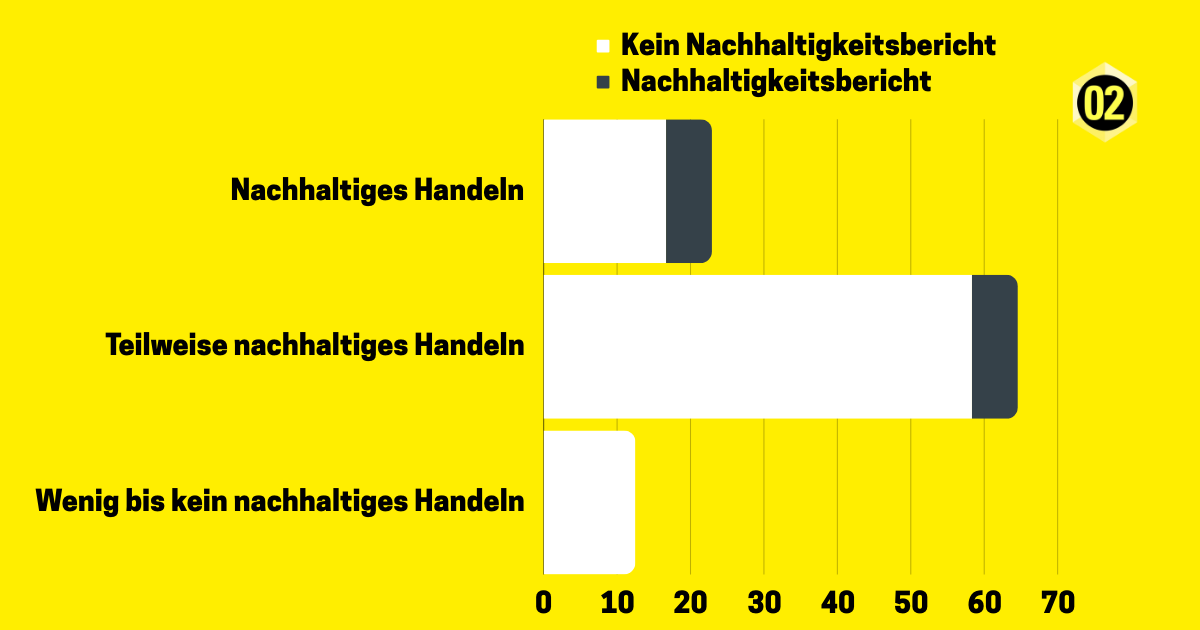

The largest group is the one in which companies act at least partially sustainably but do not report on it. The second largest group is made up of companies that already act sustainably but do not publish this information. As the results of the study show, the majority of companies practise sustainable activities, at least in part, but without communicating these efforts.infographic for sustainability report

However, making these efforts visible could have a positive impact on the relationship with the company's stakeholders. For this group, further training in the area of voluntary reporting would be a good idea.

The reason why many companies do not produce a voluntary sustainability report is that the subjectively perceived disadvantages outweigh the potential benefits for decision-makers. The survey participants see the greatest challenges in sustainability reporting in the difficulty of obtaining and processing data, in the lack of resources (e.g. financial resources, employee capacity) or in the complexity of selecting the relevant content (e.g. selection of key figures). The greatest opportunities are seen in achieving higher profit margins, increasing competitiveness and increasing employee motivation and loyalty.

In general, there is a great deal of scepticism with regard to sustainability reporting. The majority of respondents are against extending the reporting obligation to a wider group of companies. 58% of respondents do not believe there is a positive correlation between sustainability reporting and sustainable corporate behaviour. An equal number of respondents said yes and no to whether the preparation of a sustainability report makes a positive contribution.

To summarise, the results of the study show a need for further training in the area of sustainability reporting.